One of the most fascinating things about Minnesota is the infrastructure. It’s a state that was built to thrive in the cold. In the major city of Minneapolis, for example, there are nearly 10 miles of enclosed pedestrian footbridges. Referred to as the Minneapolis Skyway System, the elevated bridges and tunnels connect 80 full city blocks, giving people access to numerous downtown destinations, free of exposure to the often frigid weather.

This type of industrious, connective thinking and planning seems to be built in to the mindset of many Minnesotans. They understand the importance of staying connected despite circumstances and environmental factors. For that reason, it shouldn’t come as a surprise that Minnesota is a place where video banking has not only been adopted, but embraced.

If you went to Minnesota and visited one of Affinity Plus Federal Credit Union’s 28 locations, you’d find a robust yet humble financial institution. Their locations are concentrated in the Minneapolis and St. Paul areas, but their footprint has increased in recent years. They’ve grown to serve smaller, more disparate communities in the far reaches of the state.

Likewise, their assets have grown as well. At over $3 billion—and having grown from $2.4 billion just in the last year—Affinity Plus manages a significant amount of assets. But as a not-for-profit, member-owned cooperative, Affinity Plus isn’t only focused on their asset size. Their main focus is serving their 220,000 members. In their own words, they’re committed to “improving the lives of [their] members through meaningful banking, exceptional experiences, and trusted relationships.”

With the shuttering of branches during the COVID-19 pandemic, delivering on these key goals became difficult for Affinity Plus. But like a bridge built to connect people in a blizzard, the Minnesota credit union decided to use the adversity as an opportunity to improve their member experience. It was time for them to make the jump to video banking.

“We started looking at it pre-pandemic,” said Jenny Nubeck, director of the Affinity Plus digital branch. “We felt like it just really opened up the capabilities for our membership.” Corey Rupp, Senior Vice President of Lending, shared the sentiment. He said the pandemic hastened their launch of video banking channels, but that it wasn’t the sole motivator leading up to it. Affinity Plus was already looking for ways to better serve their members and keep them connected—no matter where they were.

When asked how willing their members were to try the new service, Nubuck said she was surprised. Adoption of the video banking channels was higher than she’d expected. “It’s surprisingly simple,” she stated. “Based on everything we’re hearing from members, they’re like, ‘Ok, don’t let this service go away.’”

According to Rupp, the willingness to adopt is tied not only to the platform’s ease of use, but also to its versatility and functionality. “We’ve been able to do everything that we do in a branch through video banking,” Rupp said. “It’s been a great experience.”

Samantha Prudhon Falkowski, a member advisor at Affinity Plus, also commented on POPi/o’s functionality. Falkowski says she generates three to four loans per week through the video banking channel. And more importantly, she takes the video calls as a chance to discuss and compare options with members. By conversing face-to-face, Falkowski can get a sense of what the member is looking for, allowing her to best advise them. “The majority of calls that I’m seeing through video banking are people who want to have that in-depth conversation about ‘What’s the best recommendation?”

By taking video calls and fielding members’ questions, Falkowski gets to restore the personal connection she shared with members before the pandemic. As she puts it, “POPi/o has allowed Affinity Plus to see members again—to see them in their own spaces, and to help them with their banking needs.”

To learn more about the adoption of video banking by Affinity Plus, watch the video case study.

For years, financial institutions have physically modernized their branch environments to direct customers out of transaction teller lines and into new self-service channels like ATMs and banking apps. The shift was designed to allow branch employees to capture and service revenue-producing activities like loans, investments, and business accounts. Some banks and credit unions executed this revenue-focused branch strategy even more efficiently by connecting customers via video to centrally located lending and other product knowledge experts.

For years, financial institutions have physically modernized their branch environments to direct customers out of transaction teller lines and into new self-service channels like ATMs and banking apps. The shift was designed to allow branch employees to capture and service revenue-producing activities like loans, investments, and business accounts. Some banks and credit unions executed this revenue-focused branch strategy even more efficiently by connecting customers via video to centrally located lending and other product knowledge experts.

Then the COVID-19 pandemic shuttered branches in nearly every community across the country and around the world. Without warning, financial institutions were forced to find new ways to capture and service those profitable relationships.

Most had already heavily invested in mobile banking apps, online applications, and highly experienced call center teams. Most thought these digital channels could replicate branch services. Most discovered that wasn’t the case.

POPi/o® experienced exponential growth in 2020, including a 283% increase in call volume. We credit that growth to many of our new clients, using video to fill that in-person service gap. These banks and credit unions didn’t invest in video banking technology as a leap of faith; long before the COVID-19 pandemic, our platform usage data had already revealed that revenue-generating activity represented more than three-fourths of total call volume. The percentage of video banking calls to support new accounts and lending compared to total video calls rose even further in 2020 to 80%.

Our 2020 user data also reveals that as branches have reopened and other delivery channels have improved, video banking usage remains high. In fact, as 2020 came to a close, video banking traffic continued to climb.

For financial institutions seeking additional new account and loan volume, this is great news. Video banking not only replaces branch service in a pinch, but it can also extend the reach of your in-person service to capture and service even more profitable relationships. This centralized operational strategy frees your most talented employees from being confined to a specific geographic location. Video banking allows your best employees to make the biggest impact on your organization, leveraging the efficiency and convenience of digital delivery to generate even more high-touch, revenue-generating activities.

For financial institutions seeking additional new account and loan volume, this is great news. Video banking not only replaces branch service in a pinch, but it can also extend the reach of your in-person service to capture and service even more profitable relationships. This centralized operational strategy frees your most talented employees from being confined to a specific geographic location. Video banking allows your best employees to make the biggest impact on your organization, leveraging the efficiency and convenience of digital delivery to generate even more high-touch, revenue-generating activities.

Educators Credit Union is a perfect example of a financial institution that had modernized branches to include centralized lending via video banking but was forced to switch gears quickly when branches closed. Because Educators Credit Union needed to deliver face-to-face service to members quickly, the credit union first deployed video banking to its website, which only required pasting a few lines of code. After some marketing across social media platforms, website video banking traffic grew enough to convince Educators Credit Union that the next step—mobile video banking would be a profitable move.

Educators Credit Union deployed a standalone video banking mobile app, rather than integrating video banking into its existing mobile banking app. Nearly all POPi/o video banking clients deploy mobile video banking this way because it allows for more rapid deployment and provides availability to non-customers to connect for new business. In fact, financial institutions that have launched video banking through existing mobile banking app integrations have often later added a standalone app to capture new business.

Looking for other video banking best implementation practices? Our phenomenal 2020 growth and influx of new institutions live on our platform has provided a treasure chest of tips and strategies for creating and deploying a successful video banking. Download our 2021 Video Banking Implementation Guide here to begin. Then, when you’re ready, click here to talk to an expert.

To learn how POPi/o Video Banking can help your financial institutions maintain relevance and personal service, request a FREE demo.

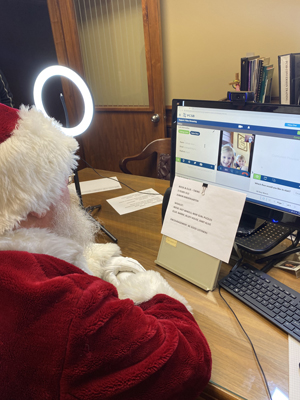

PCSB Bank has already won Christmas.

PCSB Bank has already won Christmas.

The leaders of this $1.5 billion financial institution in Clarinda, Iowa, were crushed to learn that officials had canceled this year’s community Santa House. The cancellation left no place for local kids to meet Santa, share their wish list, and pose for a photo.

Even with social distancing and frequent photoshoot wipe downs, COVID-19 has turned Santa House into a risky spreader event. While the decision made sense, CEO James Johnson felt like he had to do something. The bank couldn’t let local kids miss birthdays, graduations, summer with friends, school, trick or treating, and Santa. It was just too much.

PCSB and his team brainstormed ways the bank could help bring Santa Claus to town. The answer was our video banking.

PCSB is offering free video visits with Santa to local children using its video banking channel, which is available to customers through PCSB’s website and mobile app. The 10-minutes video chats are by appointment only. PCSB is making Santa available to both customers and non-customers. Parents can schedule visits for kids by calling the bank or filling out an online form that provides the jolly ol’ elf with important personal information that makes the moment magical.

I think this is such a great idea because it’s not only good for local kids and the community, it’s good for the bank’s bottom line, too. Here are four benefits, for starters:

Joy for local children. Sure, we love to achieve career success, but real leaders get even more fulfillment out of using their resources and influence for the greater good. They couldn’t have picked a better year to do this!“When we learned that the children in our town would miss out on meeting Santa Claus this year, we were crushed—and determined to find a way to help,” said James Johnson, CEO of PCSB Bank. “We’re thrilled to bring some merriness and cheer to all the people we know and love in this great community.”

How can you use POPi/o video banking to spread good cheer? Drop your ideas in the comments section below.

Financial institutions have had to pivot quickly this year when it comes to delivering products and services, launching new delivery channels adding to and modifying using existing ones. Even those banks and credit unions confident in their digital delivery strategies were caught off guard by the dual challenges of operating remotely and switching to entirely digital interactions.

Andy Crisenberry, SVP of eLending Solutions at real estate lending fintech Black Knight, said his firm scrambled to provide support for its remote online notarization product after COVID-19 shuttered its clients’ real estate lending offices.

“This is a great technology solution that really helps with the challenges of COVID-19, but unless your business is ready to deploy, use and support RON, you won’t be very successful,” Crisenberry told HousingWire.

All new technology produces unexpected friction. In a normal year, launches are carefully planned and include feedback that identifies friction. Yes, COVID-19 drastically increased the urgency with which firms needed to launch technology or find new ways to use existing technology. However, increasing consumer expectations for intuitive, real-time digital service had already been pushing CX modernization forward faster than expected in all sectors well in advance of the COVID-19 pandemic.

Take, for example, the $2.5 billion Educators Credit Union in Racine, Wis. Like many community FIs, Educators had already determined smaller branches, supported by video access to centralized product specialists, was the most effective strategy to serve its market. It planned an in-branch video banking launch offering auto lending, mortgage and investment services that included training, testing and weeding out of all known friction points. On March 5, the credit union excitedly opened its first modern branch featuring video banking.

Less than two weeks later, COVID-19 closed every branch lobby in the credit union’s network. Existing online and mobile banking products handled essential transactions well on a dime, but new service friction points quickly popped up, including a hasty transition for employees to work from home.

Around this time, POPi/o reached out to Educators and asked if they would like to launch video banking digitally, through the credit union’s website. Within days, the executive team approved the initiative.

While this decision seems like a no brainer, consider that it required Educators to execute a 180-degree shift in video banking strategy. Staffing and workflows had to shift; the technology would now be used to provide branch services like cashless transactions and new accounts, not specialized lending and investments. Second, staff would have to be trained remotely and access new technology from their homes. Third, because Coronavirus had blocked access to lobby branch service, time was of the essence.

The solution to this challenge was a balance of speed and CX in the form of a measured, step-by-step rollout. To begin, Educators reviewed what it did know: how to train employees on using the technology and how to provide effective service on camera. It also had staff with video experience in its existing interactive teller machine service department, a valuable resource for the video skill set.

Within 60 days, the credit union had a team trained, staged, connected and ready to serve members via video banking. Educators was ready for the next step, a soft launch. On May 19, WeCU video banking branch was open for business. The launch was purposely limited, offering video banking via a widget button on the credit union’s website only a couple of days a week. Because there was no advertising, adoption numbers were small; on the first day, only 16 video calls were completed. However, this soft launch allowed the credit union to collect ample feedback from members and employees, and then take the time to address friction before taking the next step.

After one week, WeCU was promoted on the credit union’s website and social media accounts. Traffic climbed quickly and by the end of May, in just four total days of service, Educators had completed 193 video sessions.

Feedback and adjustments weren’t just limited to friction. From the first day, members raved about being able to see credit union employees face-to-face while in lockdown. Educators capitalized on the benefit of personalization and added the video banking representative’s branch location or department to the welcome screen.

Step by step, Educators collected feedback, made adjustments, increased service hours and carefully managed channel growth. Changes during the summer included increasing service hours to Monday through Saturday, providing staff with professional lighting, staging, and more on-camera training.

Educators launched its mobile app on August 12. After a couple of weeks to work out any bugs, a marketing campaign followed. By the end of October, ECU handled 5,278 sessions.

What began as an operational pivot during the Coronavirus pandemic has developed into a popular service delivery channel that members will continue utilizing after branches resume regular service. ECU didn’t change its original video banking strategy; it expanded it. The credit union will continue to offer video banking through digital channels, while also executing its original plan to provide specialized lending and investment services in branch from centrally located staff.

The future still isn’t clear when it comes to how COVID-19 has permanently changed consumer habits, but ECU has all its delivery bases covered with the ability to provide a branch experience in person or digitally through a virtual branch. This allows the credit union to focus on the future instead of worrying about it. ECU can instead focus on enhancing video banking to improve CX and achieve new member and loan growth goals.

Like other financial institutions, the Coronavirus shutdown turned ECU’s service delivery strategy on its head. Despite the urgency of the situation, credit union leaders calmly rolled out video banking using a carefully measured approach. The result was a new delivery channel that will pay dividends for ECU and its members long after its branch network reopens.

Interested in a deeper dive into Educators’ remarkable business pivot? Click here to download ECU’s case study and learn more about the unique way POPi/o approaches your growth and service goals.

To learn how POPi/o Video Banking can help your financial institutions maintain relevance and personal service, request a FREE demo.

I’m a big fan of the convenience of digital services, unfortunately, most deployments are targeted to such narrow use cases that it doesn’t address most consumer’s needs. This is especially the case for more complex financial service products. It shouldn’t be that difficult, right? Consumers should just go to the FI’s website, find the products they want and “sign-up”, or in the model of Amazon, add the product to their “online shopping cart”. Yet as branch traffic dwindles and digital adoption grows financial institutions are finding that their “online shopping cart” abandonment rates remain sky-high.

According to research by UK-based behavioral marketing company SaleCycle, the financial sector has the highest global online shopping cart abandonment rate at 83.6%. The overall average for all sectors wasn’t much better at 75.6%.

Why so high? In general, digital channels are a one-way experience. Closing a sale has traditionally been a five-step process that requires two-way communication, which is missing in digital sales interactions.

Below are the five most common sales steps:

Research shows a variety of reasons online carts are abandoned; however, they all have one thing in common, a stalled sales process. But Video Banking can help since it provides a customer experience that combines two-way, face-to-face service with the convenience, security, and efficiency expected with digital interactions. When Video Banking is leveraged to its full potential it can become the ultimate sales channel, providing financial institutions the ability to take a customer through all five sales steps in just one call.

Let’s examine how Video Banking supports these five sales steps.

Introduction

For institutions focused on increasing wallet share, the introduction and rapport building stage are already occurring while providing service to existing customers. Video banking provides an ideal channel to discuss complex transactions, solve problems, and ultimately builds rapport that leads to additional sales. Video banking helps build trust quickly with prospective and new customers in the moment of need when facing major life events. Our customers expressed the value of providing an empathic face with video while discussing consumer loan modifications and payment plans during the recent branch closures.

Discovery

Video banking allows your customer service representative (CSR) to initiate conversations that reveal unmet financial needs, which is the purpose of the discovery step. Customized digital sales pages backed by data and artificial intelligence (AI) can perform better than general digital sales tools, but only a live CSR can listen to the customer’s needs and effectively tailor their sales pitch or presentation accordingly.

Offer

No matter how well you craft an online offer and sales page, it will never compare to a well delivered presentation by an experienced CSR. Video banking can integrate professional presentation tools that add consistency and polish to your message. And, a two-way conversation during the offer step allows CSR’s to confirm that they are matching the customer’s needs with the right features and benefits of your product.

Objections

Handling objections is where two-way communication truly shines. Data and AI can anticipate which objections a digital customer may have, but video banking has a definite advantage with two-way communication that effectively identifies objections and provides the opportunity to answer questions. Additional POPi/o tools like dynamic call routing, warm transfers make accessing the right experts easy. Plus our Positivity Coach feature allows the CSR to monitor the consumer’s reaction and adjust if emotions indicate some fear or trepidation.

Close

The most important step in making a sale is asking for the business and closing the deal. However, even expertly optimized digital sales pages convert just 20% of leads. That’s because the close step can only be completed if the previous four steps were successful. Your seasoned CSRs knows when all questions and objections have been addressed and when the time is right to close the deal.. With this step, it’s essential that Video Banking tools include workflow abilities like E-sign, document exchange, and screen share, to allow for the product purchase to be finalized before the video chat ends.

Introducing POPwelcome

It’s the extra tools and system integrations that make the POPi/o Video Banking app so robust and successful. However, not all customers have downloaded the app onto their mobile devices. For customers that are browsing an FI’s webpage, your representatives can now use POPi/o’s new POPWelcome for online or mobile chat messaging, providing a truly omnichannel experience by seamlessly transitioning the customer from text chat to video banking.

Personalized service sets community financial institutions apart from national and global competitors. However, without sales, no company can prosper and grow. No matter the size of your institution, you must provide your sales team with technology that allows them to provide the best of digital and face-to-face service, without any disruption to the five-step sales process. Video banking can provide that experience. To learn more about how quickly and effectively POPi/o Video Banking can boost your digital sales conversions, request a free demonstration with a video representative.

For more information about video banking, request a free demonstration.

© 2022 POPio Mobile Video Cloud® , LLC. View Privacy Policy.