In the last few years, our way of life and doing business has gone through tremendous changes. Businesses across the globe are undergoing “digital transformations”, altering their practices or business models to cater to the rising demand for digital services.

In 2021, the global digital transformation market size was valued at $521 billion, and is anticipating a compound annual growth rate of 19% between now and 2026. But what does this all mean? In short, the increasing use of mobile devices, smartphones, tablets and other forms of technology has brought a growing demand for advanced digital features.

Consumers are more comfortable navigating apps and web portals while dealing with businesses, and with this rise in digital fluency, consumer expectations have risen as well.

But businesses aren’t undergoing digital transformations purely to meet the demands of customers. Some have also invested in digital services because of the monetary value they provide.

Digital implementations help businesses expand their service footprint and extend their hours of operation. A transformation allows a business to leverage services through efficient online tools, negating the inconvenience of in-person meetings.

With these new practices, businesses are opening new streams of revenue while also driving brand loyalty and customer satisfaction. Studies have shown that 80% of businesses that undergo digital transformation report an increase in profits, while 85% report an increased market share. Enhanced data collection and more efficient resource management are also common benefits of digital transformation.

For businesses that sell generic, out-of-the-box products, personalization may not have to play a key role in their digital strategy. But financial institutions (FIs) have a more nuanced relationship with their customers. Because everyone’s financial situation is unique, a one-size-fits-all approach isn’t always effective in the financial services industry. As Colleen Dabbs put it on The Financial Brand, “Much more than just good targeting for offers, organizations need to engage contextually, in real time, helping customers reach their financial goals.”

But what does that kind of all-encompassing, hands-on approach look like? Translating all the services of a fully-operational branch into a functional and easy-to-use app is not an easy task.

The answer, says Jim Marous, CEO of the Digital Banking Report, is that FIs need to blend the speed and convenience of their digital tools with the friendly and personalized services of their customer-facing staff.

“Banks and credit unions must focus on building a distribution network that combines the qualities of human interaction with the power of new technologies,” Marous writes.

When it comes to targeted ads and other specified offers, data collection can be highly beneficial practices for FIs. In a survey, Mckinsey showed that triggered communications—typically featuring personalized product recommendations—contributed to 5-15% increases in revenue and 10-30% increases in marketing spending efficiency.

While those numbers alone are an incentive for FIs to be thinking about personalization in their digital marketing practices, there’s a lot more to the story. Enhanced selling isn’t the only benefit that personalization can have. As BCG stated in their publication on the topic, “Personalization in banking is not about selling, yet many banks tend to focus on the sales arena.”

Instead of being limited to the sales and marketing arena, personalization can comprise a large part of an FI’s strategy in coming years. “The combination of data, analytics, applied insights and new engagement models will open the door for an exponential increase in ideas and innovations for new products, services, engagement options and communication strategies,” writes Jim Marous.

With what he calls the “hybrid distribution model”, Marous says that banks and credit unions can meld technology and data collection with the assets provided by their customer-facing staff and their in-branch product experts.

Balancing digital self-service technology with the engagement of FI representatives has been shown to lower the abandonment rate of services like loan applications and new account openings. Instead of exiting the page when they hit a snag, these customers are given the opportunity to work with the specialist that best fits their needs.

When they can’t access a branch, yet still need to complete a banking transaction that can’t be accomplished on their own, customers need to know that their FI will still be able to serve them. In the digital world, even collaborative, in-depth banking services need to be accessible outside the branch.

By showing your customers that your FI can deliver friendly, personalized service—whether it be through web, mobile, or in-branch channels—you do more than just enhance your customer satisfaction rating. You open the door to new opportunities, securing new streams of revenue and investing in your ongoing digital relevance.

To learn more about Digital Communications and the ways it could benefit your financial institution, schedule a free demo today!

Well if that isn’t a captivating subtitle, I don’t know what is. But behind that statement is a real—and in some cases, dire—fact of digital banking services: Some of them don’t work.

Users begin processes on their phones and tablets, only to leave them incomplete. They run into snags or are told they have to visit a branch in order to proceed. So they close the app or the webpage, and leave the transaction unfinished.

Meanwhile, other digital services are able to provide the convenience and support needed to create a successful customer outcome. They give the user a host of quick and easy solutions, while also offering the full capabilities of a branch visit.

So, what does it take to make the cut? Why do some digital services outperform others? And why are digital banking services so important anyway? In this blog, we’ll take a closer look at what’s needed to offer a satisfying experience to today’s digital consumer.

Meeting consumer needs has always been a challenge for businesses. And with the recent growth and disruption of emerging technology, providing customers with satisfying experiences has become something like trying to hit a moving target.

Then, as if the situation wasn’t already complicated enough, the COVID-19 pandemic struck, profoundly affecting the standards consumers had for digital experiences. With many in-person transactions, services, and experiences shut down, consumers shifted their reliance to digital outlets. This meant that many businesses had to quickly and effectively provide a digital infrastructure to their customers.

But now digital services have become a prominent feature in the lives of many users. People have become adept at navigating various kinds of digital experiences. Because of this increase in digital adoption and user proficiency, people no longer tolerate an inefficient, frustrating user experience. They want services to be fast and comprehensive, they want their needs to be understood, and they want clear, navigable pathways to whatever they’re trying to accomplish.

After years of being well-versed in streamlined apps and online services, the average consumer has little patience for frustrations and roadblocks in the online world.

One area where these frustrations crop up is with chatbots. These tools, along with AI, automation, and self-service channels, can anger the customer, failing to understand their need, and offering no through-line to human assistance when requested.

In banking, chatbots, AI, and self-service channels may be excellent tools for simple, high-frequency interactions. But when these limited services are all a customer is offered, they can be made to feel like their FI doesn’t value them as a customer, that it doesn’t want to provide them with a solution to their problem.

Forbes noted in an article that though chatbots are being offered by an ever-increasing number of banks and credit unions, they continue to lead to fewer happy customers. Research shows that 22% of chatbot experiences lead to customers being “frustrated”, and a further 11% led to them being “angry”.

These sour experiences can erode brand loyalty, which is leading to many customers leaving their FI’s for more technologically-adept ones. This act of leaving one’s institution for another is called “customer churn”, and in the next few years, it’s expected to hit an all-time high. According to Foresight Research, the pandemic created a “hot spot of churn”. They found that customer churn increased from 12% to 22%, and is still on the rise. At some banks, it’s gotten as high as 27%, making it increasingly clear that effective digital services have become a vital aspect of customer retention.

To many FI’s, this statistic should be a canary in a coal mine. The proliferation of digital services is not a trend, it’s a shift. And the businesses that don’t adapt to it will always run the risk of being left behind.

Satisfying the digital consumer may seem like a daunting endeavor. Many FI’s are left wondering what digital services to implement, or whether the digital tools they have will still be relevant a few years from now.

But the best advice, as offered by Forbes and other outlets, is to provide a host of services, allowing users to find the appropriate level of assistance for their needs. The goal for any business in this position is to eliminate dead ends from their customers’ digital journey. If one particular point is causing hang-ups, frustrations, or high abandonment rates, it should be rethought to offer a more efficient and comprehensive pathway for the customer.

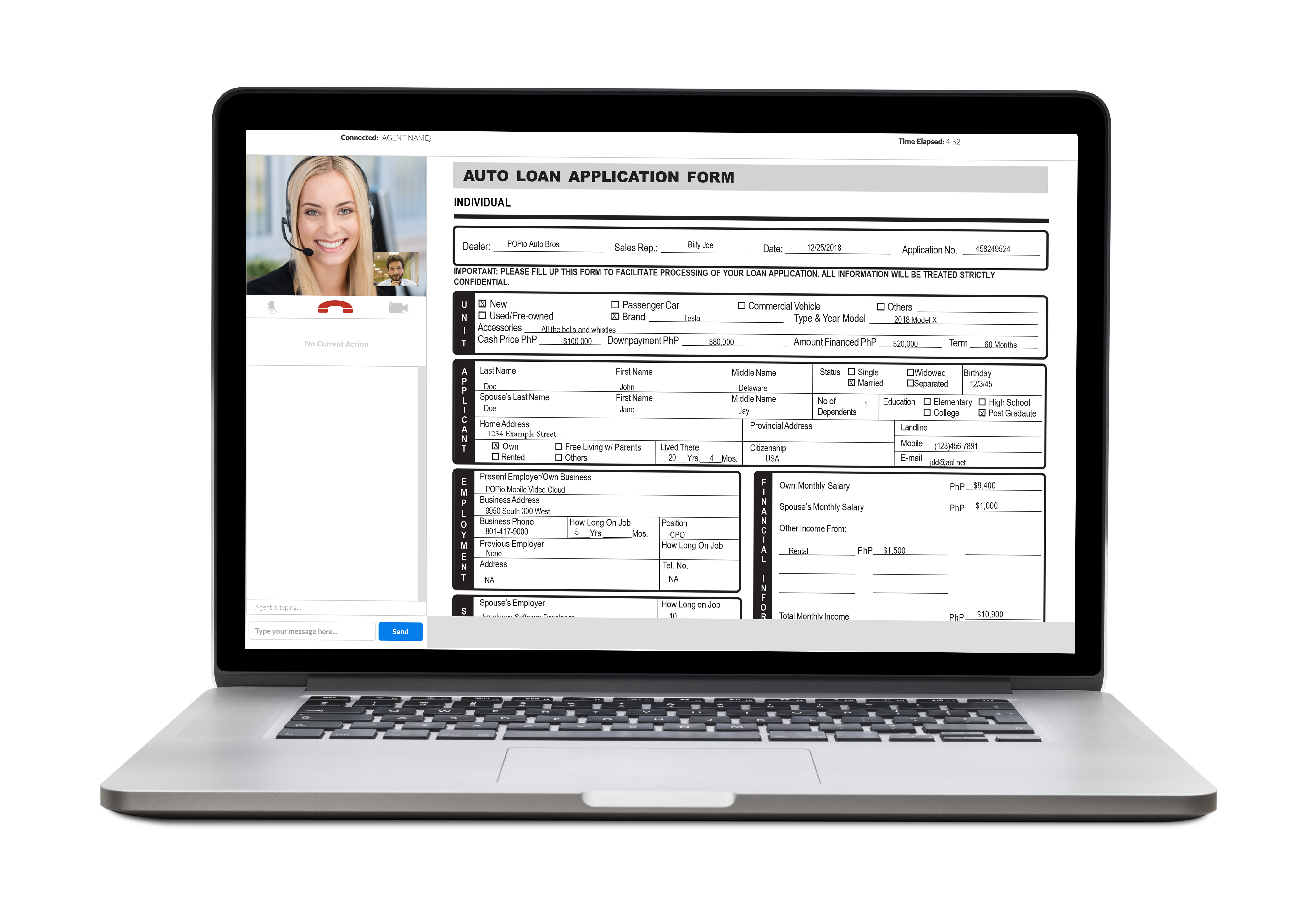

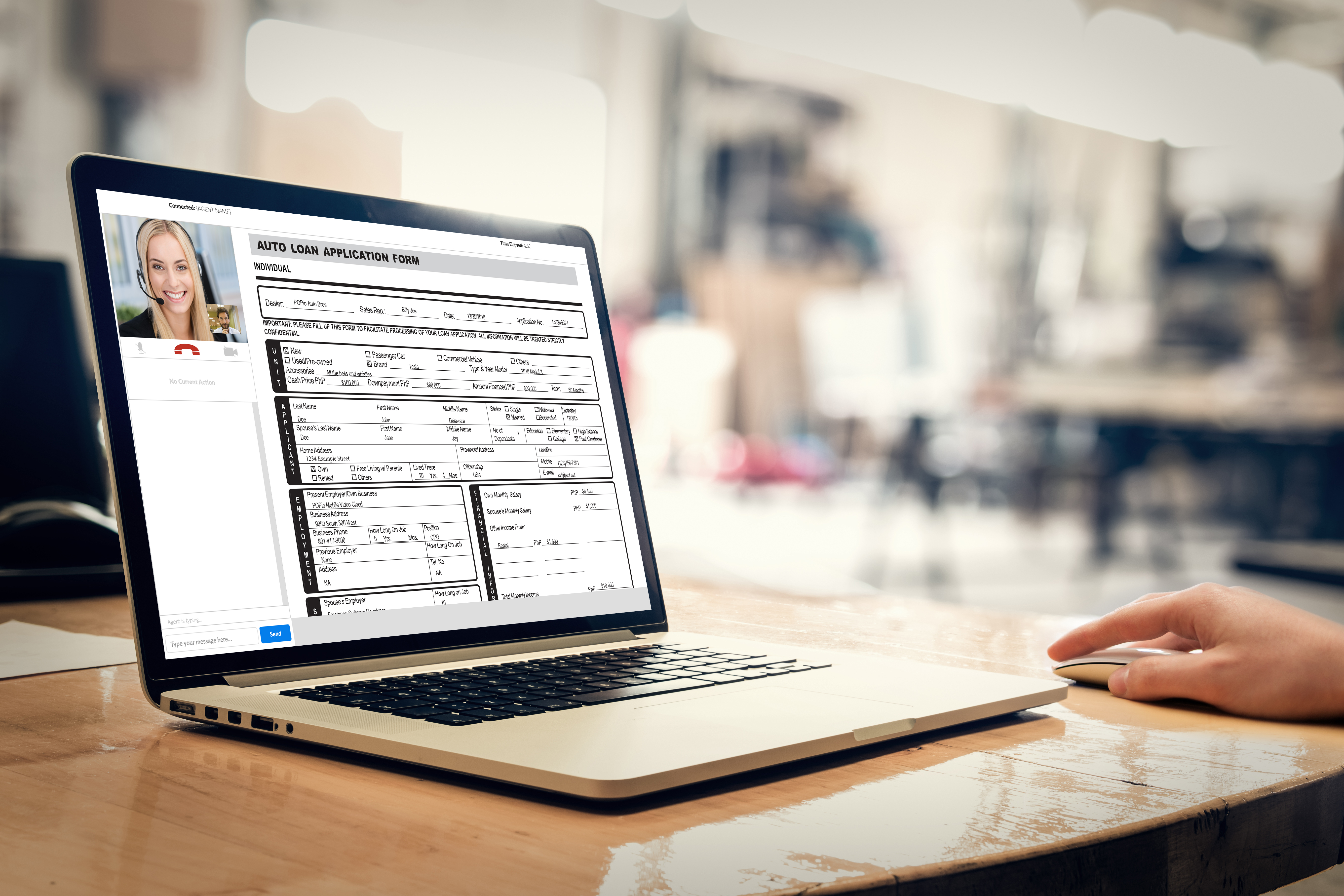

This idea especially applies to the services that banks and credit unions typically perform in branches. Applying for loans, opening new accounts, and speaking with experts about mortgages and investments are just a few examples of tasks that users struggle to complete through digital self-service channels.

According to Jim Marous, publisher of the Digital Banking Report, the baseline abandonment rate for online users opening new accounts through self-service channels is 19%, and at some FI’s it’s as high as 75-80%. Furthermore, Javelin Research found that only 8% of mobile users seeking to open a new account were able to complete the process on their phones.

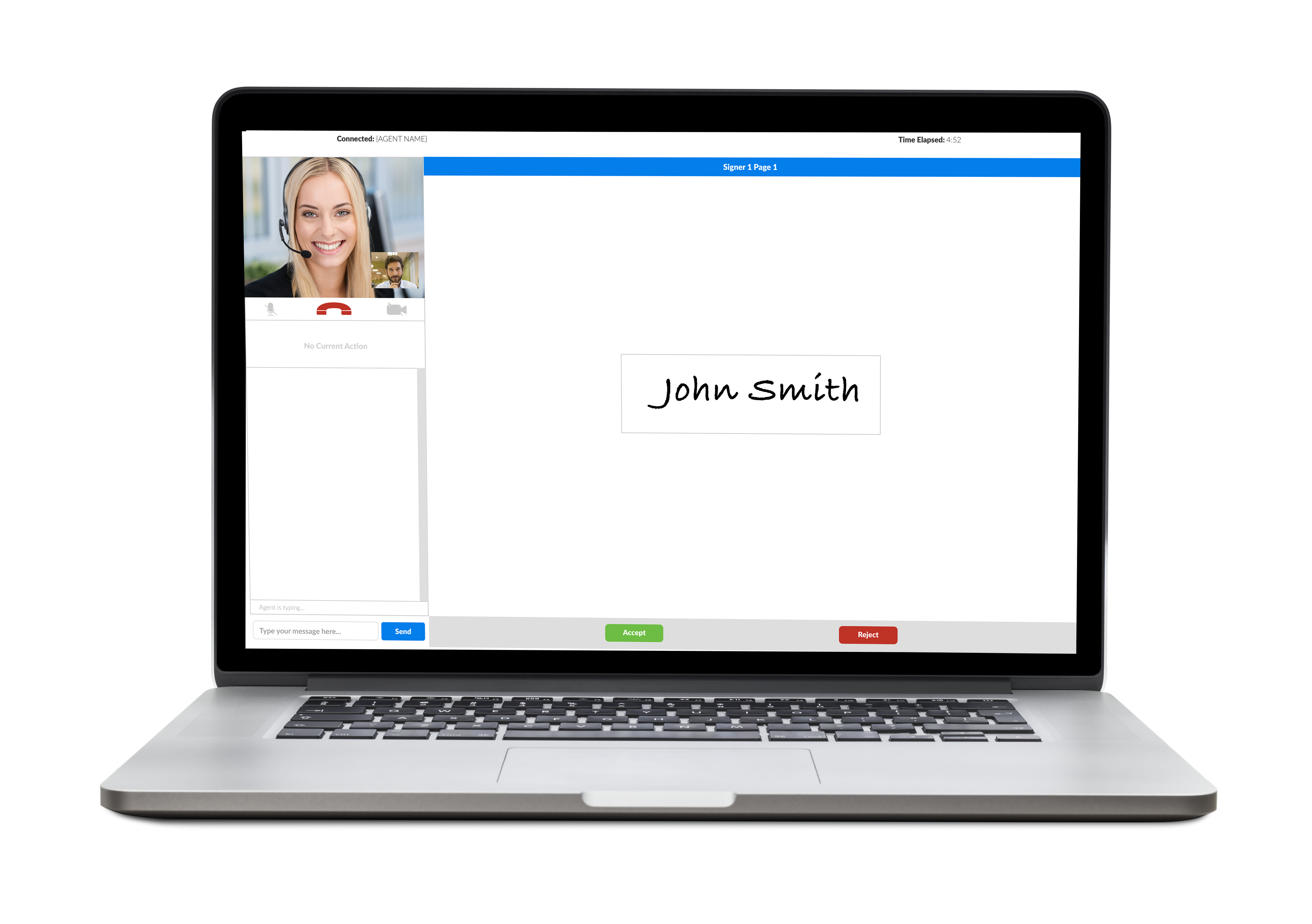

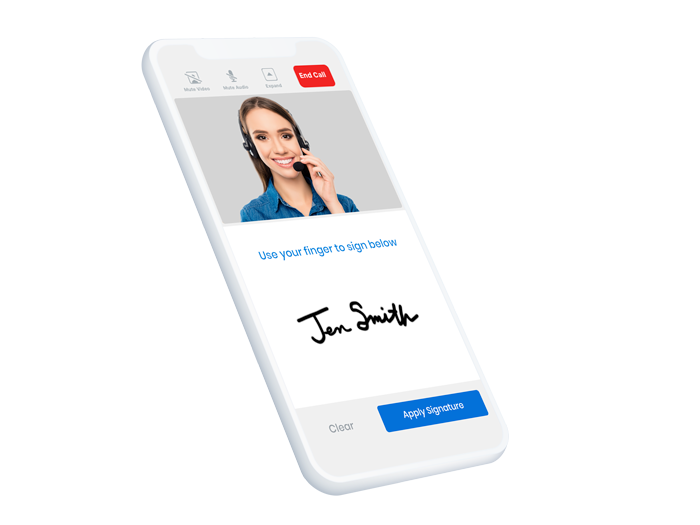

For services like these, users are calling for a “mayday” button—a direct connection to the expertise they need to complete their desired task. This option seamlessly elevates the customer from the chatbot, self-service, or call-center roadblock that they’re facing, and puts them in touch with the banking professional they need to effectively resolve their issue.

Especially helpful for loans, new account openings, and other operations that comprise the majority of a typical FI’s revenue stream, this personalized, human-to-human service improves brand loyalty and digital satisfaction.

It can be delivered over chat, voice, or collaborative video, giving users a satisfying digital alternative to the in-branch experience, and giving your FI a proven way to operate efficiently in the digital space.

At POPi/o, we know it can be tough to keep up with the changing demands of consumers. But finding an effective digital solution doesn’t have to be an arduous task. We’re here to help you discover and explore new options for managing customer relationships, because we know there’s nothing more important to you than being there for the people you serve.

If you’d like to learn more about the POPi/o Digital Communications platform, schedule a demo today.

In the late 1940’s the Shell Oil Company began providing financial services to a few of its employees. The services were limited, but employees of the oil company welcomed the idea. Because so much of their time was spent offshore or traveling, banking was—to many of them—a chore that they were glad to see simplified by their employer.

Decades later, Shell Credit Union would become Xplore Federal Credit Union, but their aim to simplify the banking experience for workers in the oil and gas industry never went away.

Xplore recently overhauled their digital offerings with the help of POPi/o. They now offer a suite of digital services, with video banking playing a key role in the implementation. In anticipation of the rollout, Xplore held an in-house contest to choose a name for their new services. The contest helped garner company interest, getting the employees acquainted with the new video banking platform. One employee suggested “Xplore Away”, which ended up taking the cake.

The credit union began offering the service to all its members free of charge. They did some marketing to build awareness, and soon, their new video banking service was garnering real interest. Today, Xplore Away boasts an impressive adoption rate. Over 67% of their memberbase has used the solution. Additionally, the majority of their new account openings are driven purely through Xplore Away.

Xplore has a modest staff of only 45 employees, which means they have to work hard to service their 8,000 members. And because a large portion of their memberbase still work in the oil and gas industry, they don’t always have the option to come visit a branch. Whether they’re out of the country, working on an oil rig, or would just rather not make a trip, Xplore Away has given them the ability to easily perform transactions or work with a financial service professional.

By connecting members directly to in-branch professionals, Xplore is able to service Member relationships in the most efficient way possible. Their loan officers, which may have been underutilized in a traditional branch setting, can quickly and effectively field calls that apply to their area of expertise. And the financial service professionals that comprise the department report that there are rarely, if ever, wait times for Xplore Away.

When you hear the Xplore Away team talking about their experiences helping members, there’s no denying that they’re glad to be a part of the department. Having the ability to serve people with the convenience of a digital platform and the personal touch of an in-branch experience creates new standards for efficiency and face-to-face service.

One of Xplore Away’s Member Advisors, Rocio Cueves, has worked at other financial institutions in the past, but she says she likes working at Xplore more. “At Xplore, it’s a little more one-on-one,” she says, smiling.

And now, with POPi/o’s unique digital banking solution, Xplore can deliver that one-on-one service to their members any time. Whether they’re calling from their living room, an oil rig in the Gulf of Mexico, or their office in the Netherlands, they still have access to the in-branch experience that makes Xplore special.

The Xplore Away team now provides a one-touch digital experience for their members, allowing them to handle everything from simple customer service inquiries to complex banking transactions.

To see the POPi/o solution in action, request a demo now.

© 2022 POPio Mobile Video Cloud® , LLC. View Privacy Policy.