One of the byproducts of the burgeoning digital age is a sharp rise in consumer expectations for efficient and convenient experiences. Both online and in-person, consumers have grown to expect streamlined shopping experiences, flexible appointment options, and seamless cross-channel interactions.

According to Salesforce, 62% of customers say experiences with one industry influence their expectations of others, and 88% expect companies to accelerate their digital initiatives. With the rapid evolution of digital services and an increasingly internet-savvy public, the average consumer is no longer tolerant of antiquated digital experiences that are full of friction and hurdles.

However, it’s obviously not always easy to provide this kind of broad and seamless service—especially when the financial services industry is facing major staffing shortages. Banks and credit unions are encouraged to invest in their digital experience, and yet in-branch service remains a prominent factor in the marketplace. Organizations push to engage through multiple channels, and this leaves some of them spread too thin to provide a satisfying consumer experience.

This is what makes a broad, omnichannel experience so vital in today’s market. By optimizing the customer journey and offering consumers various paths to the services they seek, you can not only secure more revenue, but can drive brand loyalty and customer satisfaction as well.

A vital ingredient in this process is cross-departmental collaboration. This is the assurance that all the individual departments in an organization are working in sync to create a cohesive consumer experience.

Take, for example, a community bank. With the staff of their branches, contact center, lending team, collections department, and investment department all accessible online, it follows that customers will expect to be able to move freely from one department to the next. But because these various departments are managed by different groups of people and run from different locations, the customers are sometimes faced with obstacles.

If a customer begins with a simple customer service request, and then later decides they’re curious about the bank’s auto loan offerings, their customer service agent might only be able to take them so far before transferring them to a lending officer. But when that switch happens, how efficient is it? If the customer is told to visit a branch, or to submit an application on the website, they may not follow through with their inquiry. But if the customer is simply transferred via collaborative video to meet with a lending expert, it could not only provide a more streamlined customer experience, but could also help the bank close more loans.

It’s for reasons like these that providing a satisfying digital experience has become so important. As author and customer experience expert Dan Gingiss put it, “Most companies must realize that they are no longer competing against the guy down the street or the brand that sells similar products. Instead, they’re competing with every other experience a customer has.”

With digital experiences playing an increasingly crucial role in consumer behavior, now is an ideal time to find the right Digital Communications Platform. Implementing the right digital solutions gives you the ability to build a more effective and personalized customer experience, enabling your financial institution to flourish in the digital age.

If you’re interested in learning more about the benefits of our unique Digital Communications Platform, schedule some time to speak with one of our experts here!

Since beginning our partnership with Abe.ai, creator of the Virtual Financial Assistant (VFA), we’ve been touching on this unique solution in our communications. But we’ve never really taken the opportunity to give a comprehensive look at what exactly a VFA does, and how financial institutions could wield it to their advantage—especially when used in conjunction with POPi/o’s Digital Communications solutions.

Founded in 2016 and later acquired by Envestnet | Yodlee, Abe.ai is an artificial intelligence company that’s focused on building virtual assistant products and infrastructure for the financial services industry. Banks and credit unions of all sizes use Abe.ai’s software to create AI-powered, human-like experiences to scale customer support teams and enhance the customer experience.

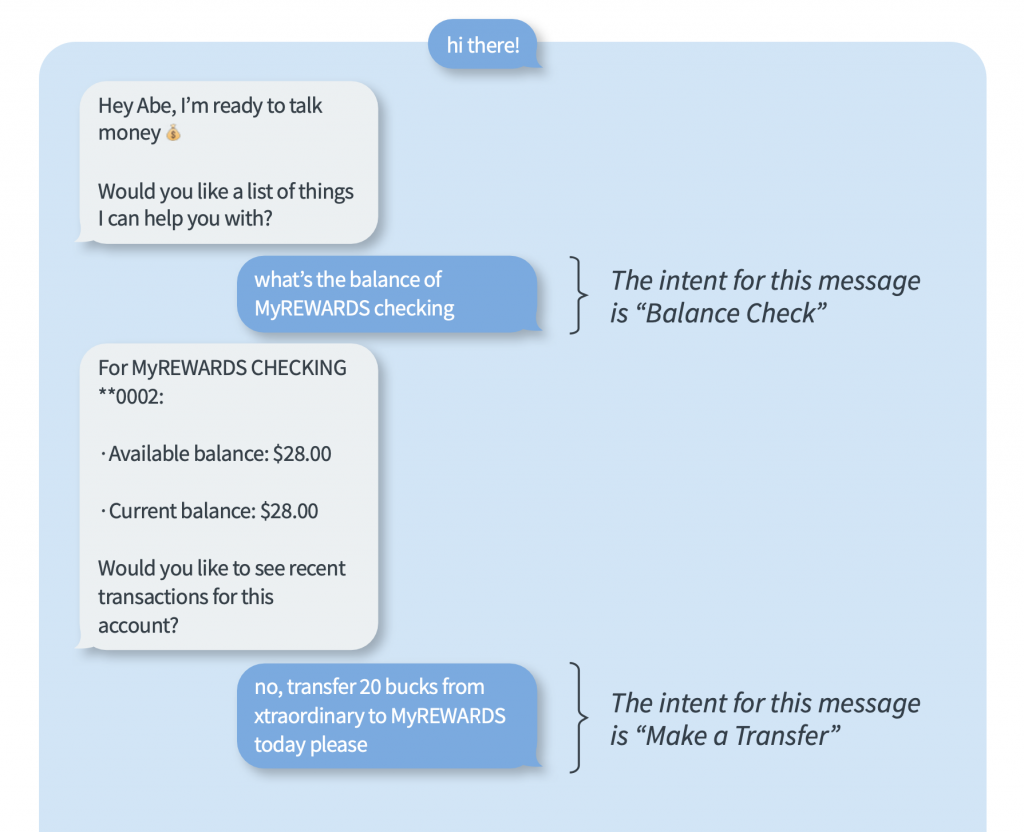

By interacting with consumers in the channels they prefer—such as website, online banking or mobile app—Abe.ai’s VFA plays the essential role of easing the load on customer service teams. Powered by machine learning and natural language processing, the VFA can interact in a natural and conversational way, resolving many common customer inquiries, freeing up call centers to use POPi/o’s Digital Communications solutions on more in-depth customer needs. With the ability to recognize thousands of utterances related to the most commonly asked questions at financial institutions, a VFA delivers a considerable amount of value to the customer experience. With a friendly, personable tone and rapid responses, it can field issues as they arise.

“I can’t remember my password.”

“What are my branch hours?”

“What’s my routing number?”

“Where’s the nearest ATM?”

“Debit card shipping time?”

“When will my deposit clear?”

“I’m locked out of my account.”

Allowing a VFA to interact with customers on behalf of your institution takes a certain level of trust. It’s important that the software meets customer needs and effectively responds to questions. But it’s equally important that your customers are willing to engage with the VFA in the first place. Making the technology approachable to the common user may seem like a tall order, but the VFA comes pre-trained right off the shelf, making it fast and easy to implement. To make the technology more engaging, financial institutions can do things like give the VFA its own name and profile image. This helps assure that the VFA comes off as friendly and approachable, and also creates an opportunity to brand it as your own. By designing a user experience that feels natural to customers, you build rapport and brand loyalty.

Looking to the Future

Looking to the FutureBecause conversational AI is a technology that continues to evolve over time, a VFA is a solution that constantly improves, providing greater value as machine learning continues to enhance its responses. And when matched with POPi/o’s Digital Communications solution, you can leverage the most convenient and comprehensive digital tools in the financial services industry. Commonly asked “nuisance questions” can be resolved without the interruption of your customer-facing staff, and more involved customer inquiries and transactions can be resolved using POPi/o’s extensive digital tools, like collaborative video, cobrowse, and more. With a Digital Communications solution, you can provide digital services that are not only fast and convenient, but friendly and personalized as well.

Are you interested in learning more about easing the load on your call centers, preventing abandonment, and meeting customer needs as they arise? Let’s talk.

In the last few years, our way of life and doing business has gone through tremendous changes. Businesses across the globe are undergoing “digital transformations”, altering their practices or business models to cater to the rising demand for digital services.

In 2021, the global digital transformation market size was valued at $521 billion, and is anticipating a compound annual growth rate of 19% between now and 2026. But what does this all mean? In short, the increasing use of mobile devices, smartphones, tablets and other forms of technology has brought a growing demand for advanced digital features.

Consumers are more comfortable navigating apps and web portals while dealing with businesses, and with this rise in digital fluency, consumer expectations have risen as well.

But businesses aren’t undergoing digital transformations purely to meet the demands of customers. Some have also invested in digital services because of the monetary value they provide.

Digital implementations help businesses expand their service footprint and extend their hours of operation. A transformation allows a business to leverage services through efficient online tools, negating the inconvenience of in-person meetings.

With these new practices, businesses are opening new streams of revenue while also driving brand loyalty and customer satisfaction. Studies have shown that 80% of businesses that undergo digital transformation report an increase in profits, while 85% report an increased market share. Enhanced data collection and more efficient resource management are also common benefits of digital transformation.

For businesses that sell generic, out-of-the-box products, personalization may not have to play a key role in their digital strategy. But financial institutions (FIs) have a more nuanced relationship with their customers. Because everyone’s financial situation is unique, a one-size-fits-all approach isn’t always effective in the financial services industry. As Colleen Dabbs put it on The Financial Brand, “Much more than just good targeting for offers, organizations need to engage contextually, in real time, helping customers reach their financial goals.”

But what does that kind of all-encompassing, hands-on approach look like? Translating all the services of a fully-operational branch into a functional and easy-to-use app is not an easy task.

The answer, says Jim Marous, CEO of the Digital Banking Report, is that FIs need to blend the speed and convenience of their digital tools with the friendly and personalized services of their customer-facing staff.

“Banks and credit unions must focus on building a distribution network that combines the qualities of human interaction with the power of new technologies,” Marous writes.

When it comes to targeted ads and other specified offers, data collection can be highly beneficial practices for FIs. In a survey, Mckinsey showed that triggered communications—typically featuring personalized product recommendations—contributed to 5-15% increases in revenue and 10-30% increases in marketing spending efficiency.

While those numbers alone are an incentive for FIs to be thinking about personalization in their digital marketing practices, there’s a lot more to the story. Enhanced selling isn’t the only benefit that personalization can have. As BCG stated in their publication on the topic, “Personalization in banking is not about selling, yet many banks tend to focus on the sales arena.”

Instead of being limited to the sales and marketing arena, personalization can comprise a large part of an FI’s strategy in coming years. “The combination of data, analytics, applied insights and new engagement models will open the door for an exponential increase in ideas and innovations for new products, services, engagement options and communication strategies,” writes Jim Marous.

With what he calls the “hybrid distribution model”, Marous says that banks and credit unions can meld technology and data collection with the assets provided by their customer-facing staff and their in-branch product experts.

Balancing digital self-service technology with the engagement of FI representatives has been shown to lower the abandonment rate of services like loan applications and new account openings. Instead of exiting the page when they hit a snag, these customers are given the opportunity to work with the specialist that best fits their needs.

When they can’t access a branch, yet still need to complete a banking transaction that can’t be accomplished on their own, customers need to know that their FI will still be able to serve them. In the digital world, even collaborative, in-depth banking services need to be accessible outside the branch.

By showing your customers that your FI can deliver friendly, personalized service—whether it be through web, mobile, or in-branch channels—you do more than just enhance your customer satisfaction rating. You open the door to new opportunities, securing new streams of revenue and investing in your ongoing digital relevance.

To learn more about Digital Communications and the ways it could benefit your financial institution, schedule a free demo today!

The pandemic has tested all of us. We’ve all changed our lives, our ways of doing business, the dynamics of our relationships, and more. For many of us, these changes have presented new challenges that have tested our patience and forced us to make sacrifices. For some of us, the cost has been far greater than an inconvenience or a missed opportunity.

And now, a full two years after this all began, the COVID infection rate in the US is the highest it’s ever been. In-person appointments are being cancelled, remote work is being enacted (or reenacted), and Financial Institutions (FIs) across the country are rolling out digital platforms to serve their customers outside the branch.

These are a few of the reasons why Digital Communications is more important than ever before. With POPi/o, your FI can deliver all your personalized, branch-based services through convenient digital channels, allowing your team to safely serve customers in a convenient and cost-effective way.

Allowing banks and credit unions to operate safely in the midst of COVID surges is only one of the ways a Digital Communications platform could help your institution navigate the current landscape. Because, along with surges, many FIs are also facing serious staffing issues. According to The Financial Brand, 80% of community banks and credit unions believe their biggest concern going into 2022 is staffing. Many branches are staffed with only one or two employees, and some are limited to drive-thru-only service.

With such limited access and so few experts to serve their customers, it’s become hard for FIs to operate efficiently. Opportunities are lost, call centers are overloaded, and product experts are underutilized. But with an effective digital platform, your FI can serve a broad customer base, even with scaled-back staffing.

Lending officers and other experts can work remotely or from a centralized location, eliminating the need to staff branches with all your product specialists. And with the integration of an AI assistant for simple customer service inquiries, you can lessen the workload for your call centers.

An effective digital strategy can not only act as a safety net from staffing struggles and COVID surges, but can also provide added benefits and new opportunities. Centralized lending departments can be enacted to make services more efficient than ever before. Expanded service hours are made possible through serving customers outside the branch. And everything from simple interactions to detailed, branch-based processes can be driven through convenient digital channels.

In an unpredictable world, FIs still need a reliable way to service customer relationships and deliver personalized services. With a Digital Communications platform from POPi/o, your FI has all the tools it needs to stay ahead of the curve—no matter what comes your way.

Ready to learn more? Let’s talk.

When Lousiana-based Xplore Federal Credit Union implemented the POPi/o platform a year ago, they didn’t know how heavily they would come to rely on it come hurricane season.

This summer, the deadly and destructive Hurricane Ida struck the struck the gulf coast, leaving many without power, food, water, and other vital resources. In the video below, Xplore President and CEO, Rafael Rondon summarizes the palpable sense of relief his credit union felt knowing they at least had POPi/o to help them continue serving members through this difficult time.

Being a Louisiana-based financial institution, Rafael and his team were no strangers to hurricanes. They had seen the damage sustained in previous hurricanes. So, when Hurricane Ida arrived, they knew they’d have to think fast to keep their members taken care of.

“Hurricane Ida hit on Monday morning,” Rafael begins, detailing the experience. “But by Friday afternoon we were up and running using POPi/o.” Watch the video below to hear more on how Xplore got up and running so quickly.

Most of what they were doing was assisting people who had evacuated the area. They were greeted with members that were grateful in the face of difficulty.

Another way POPi/o was able to help the situation was by providing the technology for Xplore’s employees to work from home during the hurricane. With POPi/o’s flexible platform, the Xplore team was still able to deliver vital services to members from outside their office.

But POPi/o also helped Xplore handle more pressing matters. Using POPi/o’s uniquely extensive capabilities, Xplore was able to provide emergency loans to members who were affected by the hurricane. In the video clip below, you can hear Rafael explain the value this service provided during his members’ immense time of need.

“Our video banking department was processing something like 120 emergency loans during those last two or three weeks of the month, after Hurricane Ida—because, you know, our members needed those emergency funds,” Rafael says, detailing the urgency of the situation they faced.

When asked if he could imagine repeating the experience without POPi/o, Rafael states plainly, “I couldn’t imagine not having POPi/o… It’s a scary thought to be honest with you.”

While members were able to receive some limited services from the credit union over their phone lines and mobile apps, only POPi/o allowed them to deliver their personalized, comprehensive services that they’re known for. To hear Rafael’s full answer, watch the video below.

And if you’re interested in learning more about POPi/o’s Digital Customer Engagement platform, talk with one of our experts.

© 2022 POPio Mobile Video Cloud® , LLC. View Privacy Policy.